Who is Revenue Share Digital For?

I partner exclusively with a small number of serious, ambitious ecommerce stores and service based businesses (£3K AOV+) such as Driveways, Roofing, Windows & Doors, Rendering & Coatings, Solar Panels, Garden Rooms, Loft/Garage Conversions, Landscaping and Fencing/Decking and want a true marketing partner — I'm someone who doesn’t just generate sales and leads, but who shares in the risk, the work, and the upside. I can only work with a select number of businesses at any one given time. Please check below to see if your business is eligible.

How I Generate Leads on Autopilot

Step 1 - High-Converting Sales Funnel

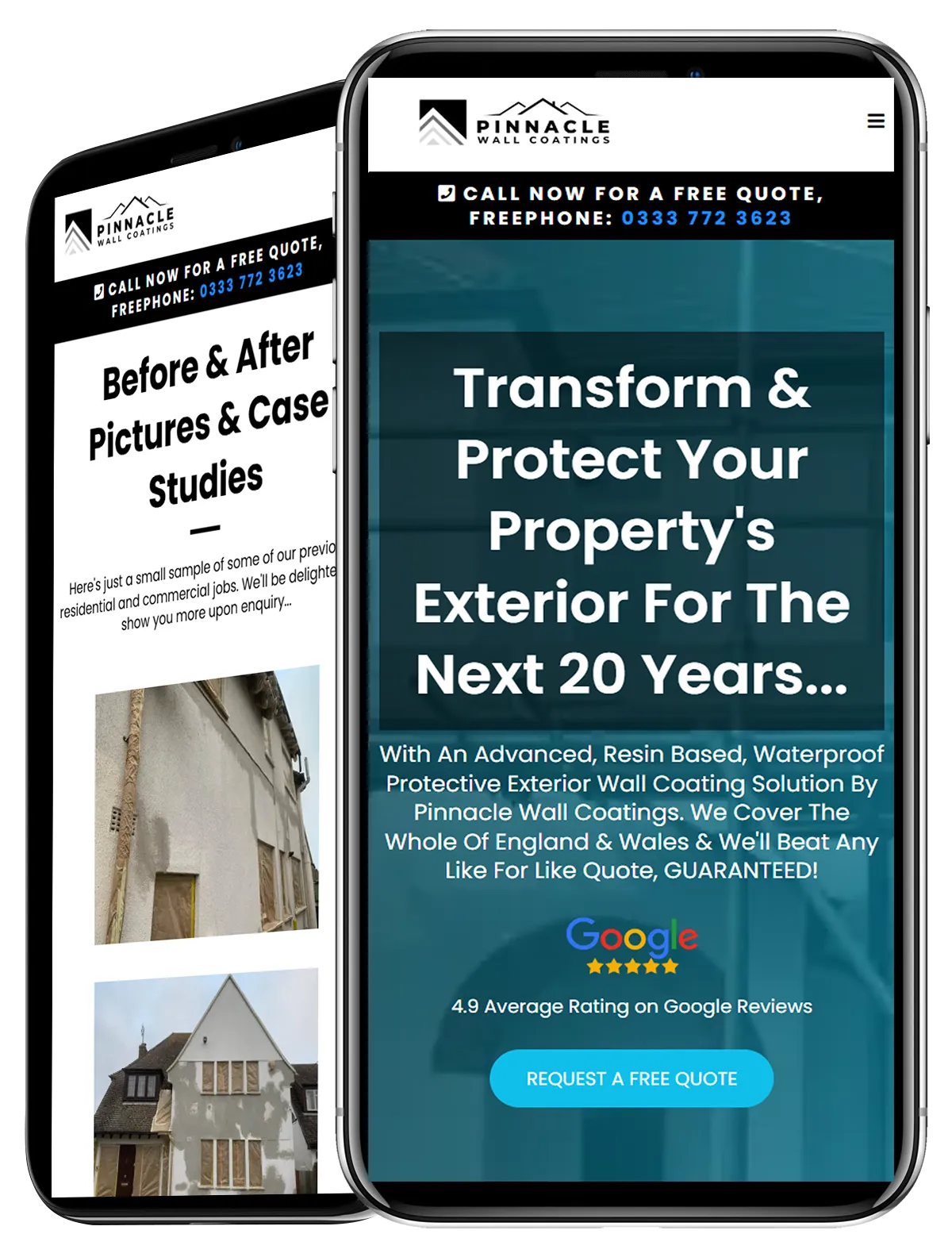

I'll design, build, host and manage high converting sales funnel for your business that turns visitors into sales.

I'll use the exact same high-converting funnel templates that I've used to generated over $3M worth of business over the last few years.

No more static 'brochure-style' websites that don't generate laser focused, highly-qualified leads.

You'll get a high converting sales funnel and website that generates

leads on auto-pilot.

Step 2 - Laser Targeted Traffic

I'll build, manage and optimise a series laser targeted SEO, Google Ads, Meta Ads, Organic Social & Automated Email campaigns to maximise your exposure across all relevant channels to attract a steady flow of highly qualified leads.

- Google Search

- Google Ads

- Facebook Ads

- Instagram Ads

And wherever else your target audience hangs out online.

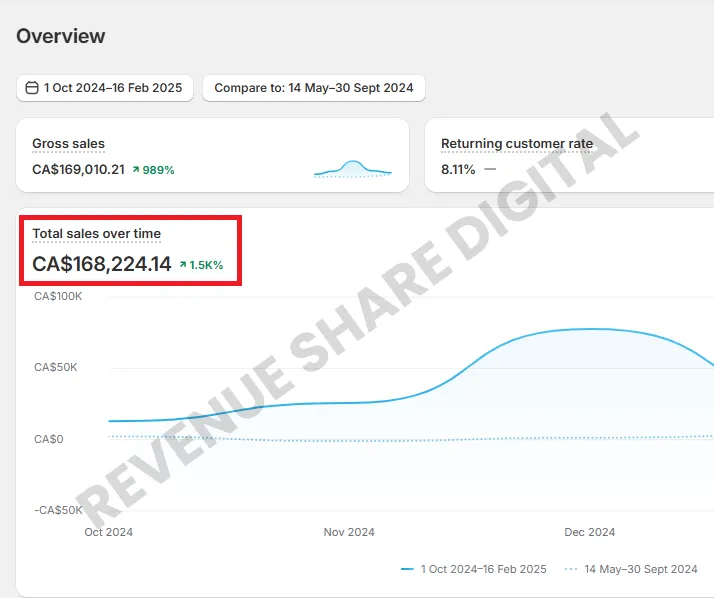

Case Studies

I can't guaranteed these results for you but it shows what could happen.

CASE STUDY

A Technology Store Has Increased Revenue by 106.1K in Just 4 Months With a 3550% ROAS

CASE STUDY

A Technology Store Has Increased Revenue by 106.1K in Just 4 Months With a 3550% ROAS

CASE STUDY

A Clothing & Apparel Store Has Increased Total Revenue by 40% in Just 4 Months

CASE STUDY

A Clothing & Apparel Store Has Increased Total Revenue by 40% in Just 4 Months

CASE STUDY

An Electronics Store Has Increased Increased Total Revenue By 1500% in 115 Days

CASE STUDY

An Outdoor Living Company Has Gone From £17K/pm To £82.6K/pm in 142 Days

CASE STUDY

An Outdoor Living Company Has Gone From £17K/pm To £82.6K/pm in 142 Days

Step 2 - Laser Targeted Traffic

I'll build, manage and optimise a series laser targeted SEO, Google Ads, Meta Ads, Organic Social & Automated Email campaigns to maximise your exposure across all relevant channels to attract a steady flow of highly qualified leads.

- Google Search

- Google Ads

- Facebook Ads

- Instagram Ads

And wherever else your target audience hangs out online.

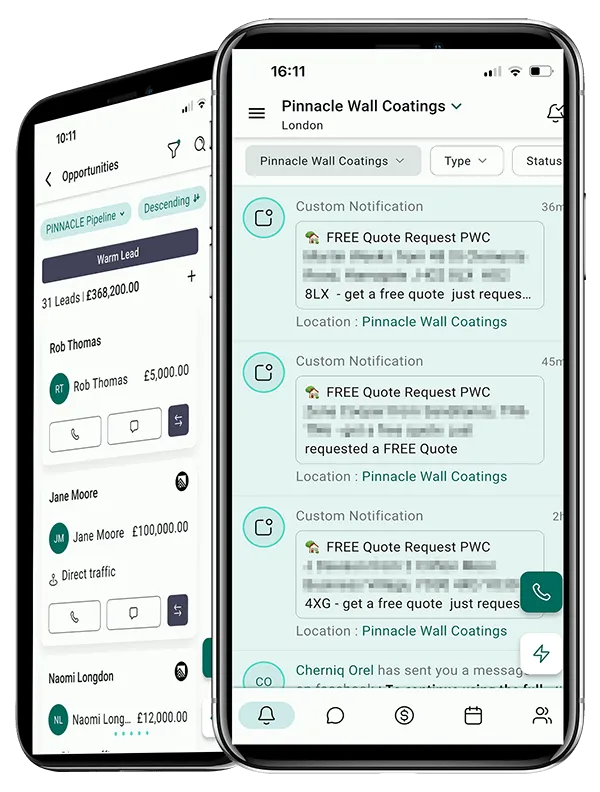

Step 3 - Lead Notifications

I'll design, build, host and manage high converting sales funnel for your business that turns visitors into sales.

I'll use the exact same high-converting funnel templates that I've used to generated over $3M worth of business over the last few years.

No more static 'brochure-style' websites that don't generate laser focused, highly-qualified leads.

You'll get a high converting sales funnel and website that generates

leads on auto-pilot.

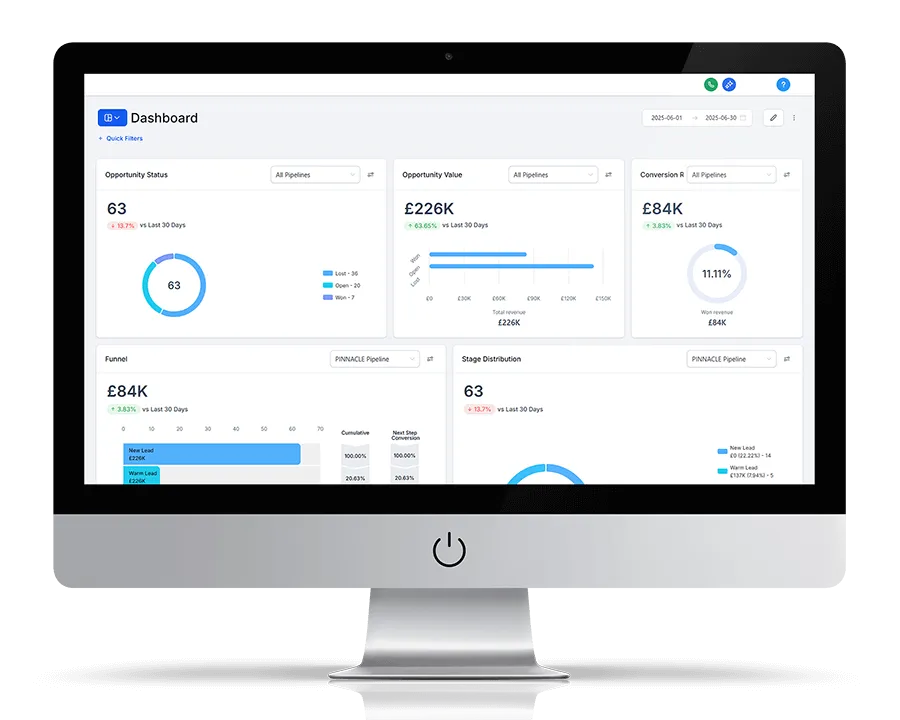

Step 4 - Performance Managment

I'll build, manage and optimise a series laser targeted SEO, Google Ads, Meta Ads, Organic Social & Automated Email campaigns to maximise your exposure across all relevant channels to attract a steady flow of highly qualified leads.

- Google Search

- Google Ads

- Facebook Ads

- Instagram Ads

And wherever else your target audience hangs out online.

Step 4 - Performance Management

I'll build, manage and optimise a series laser targeted SEO, Google Ads, Meta Ads, Organic Social & Automated Email campaigns to maximise your exposure across all relevant channels to attract a steady flow of highly qualified leads.

- Google Search

- Google Ads

- Facebook Ads

- Instagram Ads

And wherever else your target audience hangs out online.

Step 5 - Scaling & Optimisation

We work together and I scale and optimize marketing budget for consistent and predictable sales growth.

Instead of burning money on marketing, let me build you a scalable, automated customer acquisition machine that works even while you sleep and only costs you when you close leads.

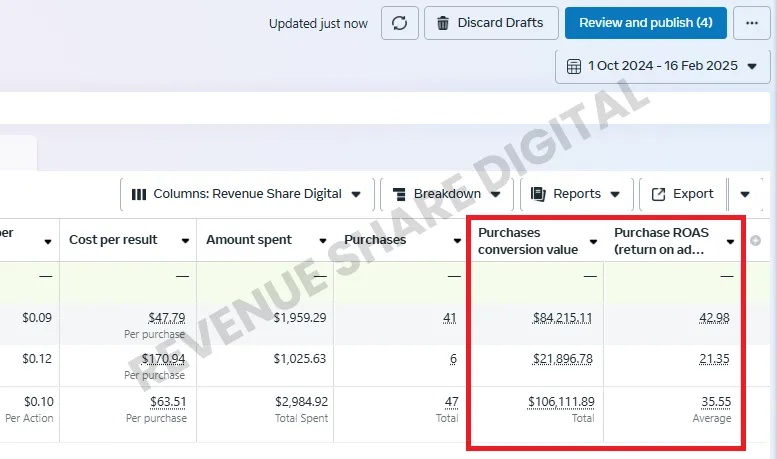

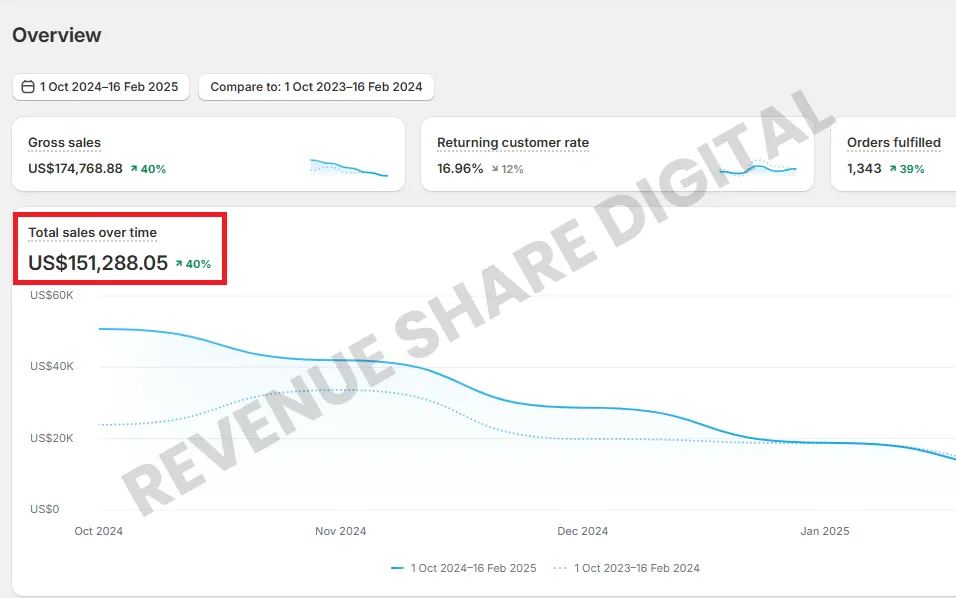

Case Study

From £17K To £100K+ Per Month In Just 3 Months

Company: An exterior wall coating company covering the whole of England & Wales.

Problem: Low converting WordPress website and had tried multiple agencies and so called experts at great expense with no success in generating leads whatsoever.

Solution: High converting sales funnel and nationwide lead generation solution with expert SEO, Google and Meta/Facebook ads optimisation and management.

Payment Option: Revenue Share

Results: 623.5% YOY Monthly Revenue Growth. Blended revenue ROAS of 2080%

"Exceptional Results"

Working with RSD completely transformed the way we win leads and new business. Before, we were stuck in a vicious circle of trying and failing with multiple agencies and inconsistent enquiries.

Within weeks of partnering, we started receiving a steady flow of high-quality, exclusive leads that were actually ready to buy—not just tyre kickers. The transparency, honesty, and attention to detail have been second to none.

What really stands out is the ROI. For every pound we’ve invested in marketing, we’ve seen many times that back in confirmed jobs.

We’ve closed projects we never would have reached without this and have added six figures to our monthly turnover.

If you’re serious about growing your business, this isn’t just another ‘lead gen service’—it’s a true partnership. RSD delivers exactly what it promises, and I honestly can’t recommend this partnership highly enough."*

— J. Jackson, Partner - Pinnacle Wall Coatings

Exclusive vs Shared Motor Vehicle Accident Leads: A Strategic Decision Framework for Growth-Focused Law Firms.

By K Atkinson.

Founder, MVA Leads Direct

Specialising in state-level personal injury acquisition and scalable MVA case infrastructure

Overview.

The decision between exclusive MVA leads and shared motor vehicle accident leads is not a pricing comparison. It is a structural acquisition decision that affects cost stability, intake pressure, capital exposure, and long-term portfolio scaling.

Most discussions reduce the topic to cost per lead. Serious firms evaluate it through a different lens: cost per retained case under stress.

Shared distribution introduces competitive compression at intake. Exclusive distribution removes distribution competition but increases capital intensity. Neither model is inherently superior. Each redistributes risk differently across the acquisition system.

The firms that scale successfully do not ask which model is cheaper. They ask which model aligns with their organisational capability, state footprint, intake discipline, and tolerance for volatility.

This paper examines that decision at system level.

For broader acquisition mechanics, see: How Motor Vehicle Accident Lead Generation Works.

Table of Contents.

01 - Why Distribution Structure Matters Strategically

02 - The Economic Architecture Behind Both Models

03 - Structural Mechanics Beneath the Surface

04 - State-Level Variance: Geography Changes the Equation

05 - Operational Conversion & Intake Implications

06 - Risk & Failure Conditions

07 - How Intake Conversion Changes Everything

08 - When Exclusive vs Shared Makes Strategic Sense

To Summarize

FAQ's

01

State-Level Variance: Geography Changes the Equation.

Distribution structure changes the physics of conversion. In a shared model, a prospect’s enquiry is delivered to multiple firms. Contact race begins immediately. Intake velocity becomes decisive. Competitive pressure is externalised at the call level.

In an exclusive model, the enquiry is routed to a single firm. Competitive pressure shifts from intake race to capital allocation discipline.

This distinction matters because it determines:

- How fragile close rate is under delay

- How sensitive economics are to staffing fluctuation

- How predictable monthly retained case cost becomes

- How scaling behaves under volume expansion

Shared shifts pressure into operations. Exclusive shifts pressure into capital modelling. Understanding that pressure shift is the beginning of strategic clarity.

02

Why Distribution Structure Matters Strategically.

The only meaningful evaluation metric is cost per retained case.

Shared may cost approximately $150–$350 per lead depending on state and filtering depth. Exclusive commonly ranges $400–$900+ in competitive jurisdictions such as California or Florida.

At surface level, shared appears economically efficient. But the decisive variable is close-rate stability.

Base Case Comparison

Assume:

- Shared lead cost: $250

- Exclusive lead cost: $600

- Shared close rate: 12%

- Exclusive close rate: 16%

Shared retained case cost:

$250 ÷ 0.12 = $2,083

Exclusive retained case cost:

$600 ÷ 0.16 = $3,750

In base case conditions, shared appears superior. However, base case conditions rarely persist under competitive stress.

03

Structural Mechanics Beneath the Surface.

Shared distribution introduces what can be described as contact compression. Multiple firms receive the same prospect within minutes. The first firm to establish communication often controls the outcome. Close rate becomes tightly correlated with response speed.

Exclusive removes compression but increases reliance on conversion discipline and accurate case-value modelling.

The mechanics differ:

Shared model mechanics:

- High response-time sensitivity

- Elevated intake staffing dependency

- Volatile close-rate variance

- Lower capital intensity per enquiry

Exclusive model mechanics:

- Reduced intake race pressure

- Higher capital exposure per enquiry

- More predictable contact ownership

- Greater sensitivity to close-rate overestimation

These mechanics shape organisational requirements.

04

State-Level Variance: Geography Changes the Equation.

Distribution performance does not scale uniformly across states. In highly competitive states such as Florida and California, shared compression is amplified. Intake races are aggressive. Close-rate volatility increases.

In mid-market states such as Georgia or Pennsylvania, competitive intensity may be lower. Shared models can perform efficiently if intake is structured.

In segmented markets like Texas, performance varies by metro. Primary metros may behave like high-density states, while secondary markets resemble mid-market dynamics.

Blended national averages conceal these differences. State segmentation is mandatory.

05

Operational Conversion & Intake Implications.

Shared distribution magnifies intake velocity. If response drifts from minutes to hours, close rate can decline sharply. Even a two-to-three-point drop materially alters retained case cost.

Exclusive distribution reduces race pressure but does not eliminate operational dependency. Intake discipline remains critical. However, close-rate variance tends to be less sensitive to minor delays.

Shared requires:

- Immediate call attempts

- Structured day-one cadence

- Adequate staffing under volume

- Clear qualification scripting

Exclusive requires:

- Accurate modelling of case value

- Stable intake conversion processes

- Capital tolerance for higher CPL

The model that wins depends on operational maturity.

06

Competitive Market Dynamics.

Shared models embed competitive behaviour at the intake layer. Firms compete in real time for prospect attention. Brand positioning can be diluted if prospects perceive multiple calls as commoditised solicitation.

Exclusive models relocate competition to the acquisition layer. Firms compete financially rather than operationally.

This distinction influences:

- Client perception

- Brand positioning

- Long-term referral impact

- Attorney time allocation

In high-density states such as New York, brand alignment may influence which model better supports long-term positioning. Distribution structure is not just economic. It is strategic.

07

Risk & Failure Conditions.

Distribution structure rarely fails because of the model itself. It fails because of organisational misalignment.

Shared and exclusive leads redistribute risk differently. When firms misunderstand where that risk sits — or model it incorrectly — margin erosion begins quietly and compounds over time.

Failure is usually modelling error, not model flaw. Let’s examine how that happens.

When Shared Distribution Fails

Shared leads are not inherently unstable. They are structurally sensitive. Their failure modes are operational.

1. Intake Delay and Conversion Compression

Shared environments introduce competitive contact pressure. Multiple firms receive the same enquiry within minutes. Close rate becomes tightly correlated with response velocity.

When intake response drifts from immediate to delayed — even by 20–30 minutes — close rate does not decline gradually. It compresses.

A shared program that converts at 13% with disciplined response may drop to 9% under mild delay. That four-point shift can increase retained case cost by thousands across a monthly cohort.

What makes this dangerous is that the lead cost does not change. The decline is invisible unless retained case modelling is segmented properly.

Shared does not tolerate operational complacency.

2. Staffing Inconsistency Under Scale

Shared volume magnifies operational strain.

When volume increases:

- Call attempts cluster

- Follow-up cadence slips

- Qualification consistency degrades

- Intake fatigue sets in

Close rate drift often follows increased volume — not because the lead quality changed, but because intake capacity did not scale proportionally.

Firms frequently misdiagnose this as a “lead quality issue” when it is a staffing elasticity issue. Shared distribution amplifies internal inconsistency.

3. Scaling Beyond Operational Capacity

When shared volume is scaled aggressively without modelling staffing bandwidth, response compression compounds.

Consider a firm capable of handling 40 leads per week efficiently. Scaling to 80 without intake expansion can degrade response time, consultation scheduling, and follow-up quality.

The result is margin erosion masked as acquisition inefficiency. Shared fails fastest under overextension.

4. Optimistic Close-Rate Assumptions

Shared economics often look attractive at 13–14% close rate. But if modelling assumes 14% and actual performance drifts to 10%, retained case cost increases 40%.

That gap is rarely stress-tested before scaling.

Shared fails when close-rate assumptions are optimistic rather than stress-modelled.

When Exclusive Distribution Fails

- Exclusive distribution introduces a different risk architecture.

- It removes intake race compression but increases capital exposure.

- Its failure modes are financial rather than operational.

1. Miscalculated Case Value

Exclusive leads often carry higher cost per lead. Their viability depends on realistic case-value modelling.

If firms overestimate average settlement or fee yield, the retained case cost threshold may be set incorrectly.

Under that miscalculation, exclusive programs appear viable — until real revenue data is reconciled.

The failure is not conversion. It is valuation error.

2. Close-Rate Overestimation

Exclusive environments often convert at higher rates than shared — but not automatically. If modelling assumes 18–20% conversion but actual close rate stabilises at 14–15%, retained case cost may exceed internal tolerance.

Because CPL is higher, even minor close-rate miscalculations materially impact capital efficiency.

Exclusive requires conservative modelling discipline.

3. Insufficient Capital Tolerance

Shared distribution spreads risk across more enquiries at lower unit cost. Exclusive concentrates risk at higher unit cost.

If capital reserves or cash-flow tolerance are tight, short-term conversion variance can create discomfort, leading firms to prematurely abandon viable programs.

Exclusive fails when capital expectations are short-term rather than portfolio-based.

4. Failure to Segment by State

Exclusive performance varies significantly across jurisdictions.

In high-density states such as Florida or California, exclusive may stabilise modelling. In mid-market states, it may not justify higher unit cost.

Firms that blend state performance and evaluate exclusive nationally often misinterpret its viability.

Exclusive fails when state segmentation is ignored.

Shared vs Exclusive: Where Both Fail

Both models collapse under the same conceptual mistake:

Evaluating performance on cost per lead instead of cost per retained case.

Cost per lead is a surface metric.

Retained case cost is the economic reality.

When firms optimise for lower CPL without modelling close-rate sensitivity, they often widen qualification filters, increase intake strain, and degrade conversion stability.

When firms chase higher close rates without modelling case-value variance, they can overspend on capital intensity.

The failure pattern is consistent:

- Optimistic assumptions

- No stress testing

- Blended state evaluation

- Reactionary scaling decisions

- Neither shared nor exclusive is structurally flawed.

- But both require disciplined modelling.

The Deeper Truth

Distribution model failure is rarely caused by the external provider.

It is caused by:

- Organisational overconfidence

- Incomplete stress modelling

- Capital impatience

- Inconsistent intake discipline

- Geographic under-segmentation

The firms that scale successfully under either model share one characteristic:

They treat distribution structure as an economic system, not a lead source.

08

Scaling & Portfolio Strategy.

As firms scale, model behaviour changes.

Shared volume increases operational strain. Response-time degradation can create margin erosion. Close-rate compression compounds over volume.

Exclusive scaling increases capital exposure. Margin depends on conversion stability.

Sophisticated firms often deploy hybrid portfolios:

- Exclusive in saturated states like California

- Shared in balanced states like Georgia

- Monthly retained-case evaluation segmented by jurisdiction

- Capital allocation adjusted by state performance

- Hybrid strategies require disciplined measurement.

Without segmentation, hybrid creates confusion.

09

When Exclusive vs Shared Makes Strategic Sense.

The question is not which model is better.

The question is which model aligns with the organisational architecture of the firm deploying it.

Exclusive and shared distribution are not ideological choices. They are structural allocations of risk.

The firms that scale successfully under either model do so because the distribution structure matches their operational discipline, capital tolerance, state footprint, and competitive positioning.

Let’s examine what that alignment looks like.

When Exclusive Distribution Makes Strategic Sense

Exclusive distribution tends to align with firms that value modelling predictability over operational race dynamics.

In highly competitive metros such as California or Florida, shared intake environments can become aggressively compressed. Multiple firms contact the same prospect within minutes. Conversion becomes sensitive to seconds, not hours.

For firms prioritising brand positioning and controlled client experience, this environment can feel inconsistent with their identity.

Exclusive distribution often stabilises that volatility. But exclusivity is not about comfort. It is about capital philosophy. Firms suited to exclusive models typically share several characteristics:

- They understand their average case value with precision.

- They model retained case cost conservatively.

- They are comfortable deploying higher capital per enquiry.

- They have stable intake conversion processes.

- They segment performance by state rather than blending data nationally.

Exclusive makes sense when leadership prefers capital intensity to operational compression.

In other words:

Instead of competing through speed, the firm competes through controlled conversion.

That trade-off can produce more predictable monthly economics in saturated markets — particularly where shared close-rate volatility becomes difficult to stabilise.

However, exclusive only works when close-rate assumptions are realistic and case-value modelling is disciplined. Without those, higher CPL amplifies error.

Exclusive is not safer.

It is differently exposed.

When Shared Distribution Makes Strategic Sense

Shared distribution rewards operational excellence.

In balanced markets with moderate competition density — such as certain regions within Georgia or Pennsylvania — shared models can produce efficient retained case cost if intake velocity is disciplined.

Shared aligns with firms that:

- Maintain aggressive response-time standards.

- Staff intake proportionally with volume.

- Operate structured day-one follow-up cadence.

- Accept competitive intake environments.

- Prefer lower capital exposure per enquiry.

- Shared shifts competitive pressure from capital allocation to operational execution.

Firms that excel under shared models often view intake as a competitive advantage. They treat response time as strategic leverage rather than administrative function.

When properly staffed and segmented by state, shared can outperform exclusive on retained-case economics — particularly when close-rate stability is maintained above mid-teens levels.

But shared becomes fragile when intake discipline drifts or volume scales beyond operational bandwidth.

Shared is not cheaper.

It is more operationally leveraged.

The Strategic Decision Framework

Choosing between exclusive and shared distribution should never begin with price comparison.

It should begin with a structured evaluation of organisational capability and state segmentation.

A disciplined decision process typically includes:

- First, modelling retained case cost by state — not nationally blended.

- Second, stress-testing close-rate assumptions by at least ±3 percentage points to measure sensitivity.

- Third, evaluating actual intake response velocity under real volume, not ideal scenarios.

- Fourth, confirming staffing elasticity under projected scaling.

- Fifth, defining an acceptable retained-case cost ceiling based on realistic case-value assumptions.

When firms skip these steps, distribution decisions become reactive. When firms apply them, distribution becomes strategic.

Some organisations ultimately adopt hybrid portfolios — deploying exclusive in saturated metros while utilising shared in balanced jurisdictions. This approach can stabilise risk across states, provided segmentation discipline exists.

If you are evaluating structural fit across your state portfolio and want to model distribution alignment against intake maturity and capital tolerance, begin with the Assessment process.

The correct model is rarely universal. It is contextual. And the context is organisational capability, not ideology.

To Summarize.

Exclusive and shared MVA leads redistribute risk differently. Shared lowers capital intensity but increases operational compression risk.

Exclusive increases capital intensity but reduces competitive contact volatility.

The correct choice depends on:

- Organisational capability

- Intake velocity

- State-level competitiveness

- Capital tolerance

- Retained-case modelling discipline

Firms that segment by jurisdiction and scale within stress-tested thresholds can succeed under either structure.

Firms that rely on surface-level cost comparison will struggle. For broader acquisition context, review

How Motor Vehicle Accident Lead Generation Works.

Frequently Asked Questions.

01

Is exclusive always better in competitive states?

Not always, but more often that not yes and it often stabilises modelling when intake race compression becomes extreme.

02

How should we test?

Test by state. Segment results. Avoid blended evaluation.

03

Does brand positioning matter?

Yes. Distribution environment influences client perception.

04

What is the biggest modelling mistake?

Assuming close-rate stability without stress testing.

05

How long before scaling?

Long enough to confirm stable retained-case economics by jurisdiction.

06

Should hybrid be default?

Only if measurement discipline exists.

07

What metric governs the decision?

Cost per retained case segmented by state.

This service is not designed to be everything for everyone. It is built for firms that take inbound acquisition seriously and measure success where it actually matters — at the case level.

Blog.

MVA acquisition is not a marketing tactic — it is an economic system. While pricing is set at the lead level, outcomes are determined downstream by intake execution, follow-up velocity, qualification discipline, and cost-per-retained-case modelling. This section explores the operational mechanics behind scalable motor vehicle accident lead generation for growth-focused personal injury firms.

How Motor Vehicle Accident Lead Generation Works for Growth-Focused Law Firms.

Motor vehicle accident lead generation is not simply about buying names and phone numbers. It is a structured acquisition system designed to deliver intake-ready case opportunities at a predictable cost per retained case...

PPC vs Buying MVA Leads: Which Model Actually Scales for Personal Injury Firms?

For established personal injury firms, the PPC versus bought-leads debate is rarely philosophical. It’s operational. Both models can produce signed cases. Both models can also quietly bleed margin...

Cost of Motor Vehicle Accident Leads: What PI Firms Should Really Expect to Pay.

A $350 lead with poor intake conversion can be more expensive than a $700 lead that converts consistently. A high-cost state with strong case value may outperform a lower-cost state with weaker recoveries...

Exclusive vs Shared Motor Vehicle Accident Leads: A Strategic Decision...

The decision between exclusive MVA leads and shared motor vehicle accident leads is not a pricing comparison. It is a structural acquisition decision that affects cost stability, intake pressure, capital exposure, and long-term portfolio scaling...

03

Blog Post Title Goes Here

At scale, MVA campaigns stabilise around a 15% close rate when intake is consistent and volume is sufficient. This reflects real-world performance across competitive U.S. markets, factoring in normal variation in traffic quality, response times, and follow-up — not idealised conditions or short-term tests.

04

Blog Post Title Goes Here

A $2,000 - $2.5K case cost represents sustainable, all-in acquisition at scale, absorbing normal CPL volatility and seasonal swings. It reflects outcome-level performance where experienced buyers measure success — at the signed case, not the lead.

Start With a Controlled Validation Trial...

Before scaling, lead delivery begins with a controlled initial meaningful volume designed to validate quality, intent, and operational fit under real intake conditions — with your team, your routing, and your cadence.

There is no long-term obligation. The trial exists to confirm that lead quality, delivery speed, and conversion dynamics align with your firm’s expectations before increasing volume or expanding into additional states.

Minimum trial investment: $15,000+ upfront.

This is not a proof-of-concept. It is a structured validation period with clear parameters and measurable outcomes.

Exclusive leads - no sharing.

Intent strength at meaningful volume.

Delivery speed into your intake workflow.

Operation fit before committing to higher volume.

No retainers - no long term lock-ins.

Following the initial delivery period, pacing and volume can be adjusted based on performance, intake capacity, and commercial fit. This may include increased lead volume, modified delivery parameters, or expansion into additional states.

The objective is simple: predictable, scalable MVA lead supply — without unnecessary risk on either side.